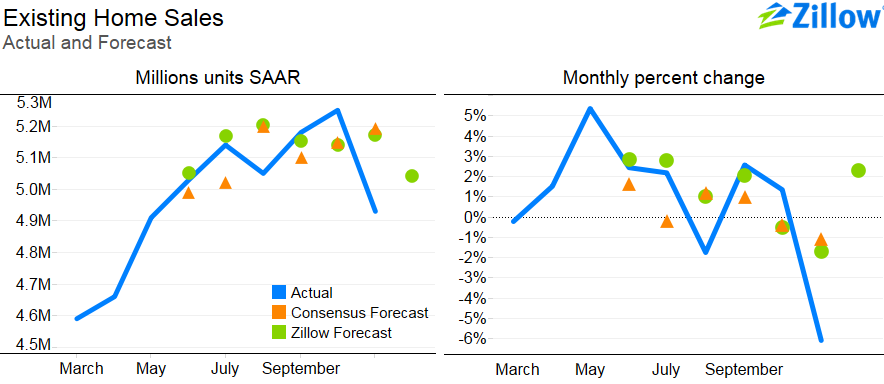

Zillow expects existing home sales to rise 2.3 percent to 5.04 million units (SAAR) in December.

- The combination of falling interest rates and gradually improving mortgage credit availability should be just enough to offset the effects of a rising homeowner vacancy rate and a still-falling homeownership rate during the third quarter.

The effects of the large unexpected drop in November’s existing home sales is expected to outweigh effects from flat pending home sales over the past five months, modestly boosting sales in December

Zillow expects Friday’s existing home sales data from the National Association of Realtors (NAR) to show an increase of about 2.3 percent to a seasonally adjusted annual rate (SAAR) of 5.04 million units in December, up from 4.93 million units (SAAR) in November.

Background

2014 was a fairly good year for existing home sales, which trended up for the year. Sales reached their highest level in October at 5.25 million units (SAAR), recovering almost all of the decline experienced during the second half of 2013 when interest rates rose. November’s 6.1 percent decline caught most people by surprise.

Falling interest rates throughout the year provided a modest and waning boost to sales: the 30-year fixed mortgage interest rate fell from 4.4 percent in January to 3.9 percent by the end of December.

However, the homeownership rate and homeowner vacancy rate tempered these positive movements. The homeownership rate fell slightly by 0.75 percentage points between January and September. The homeowner vacancy rate trended down for the first half of the year, but reversed course during the third quarter. Overall, the underlying fundamentals of the housing market remained relatively stable throughout 2014.

Forecast

Our existing home sales forecast uses a best-fit combination of two models, a structural model and a historical model. Both models point toward slightly higher home sales in December, although the structural model suggests a smaller increase.

The structural model suggests a slight increase in existing home sales of only 0.4 percent to 4.95 million units (SAAR). Unlike new home sales, the combination of falling interest rates and a relatively low level of financial stress suggested by the Kansas City Federal Reserve Financial Stress Index should be just enough to offset the effects of a rising homeowner vacancy rate and falling homeownership rate experienced during the third quarter. If interest rates had remained at their November level, thus suggesting a larger mortgage credit demand increase, the structural model would predict existing home sales to be about 10,000 higher at 4.96 million units (SAAR), an increase of 0.6 percent.

The historical model, however, suggests a larger increase in existing home sales of 2.6 percent to 5.06 million units (SAAR). The effect of the large unexpected drop in November’s existing home sales is expected to outweigh effects from flat pending home sales over the past five months, resulting in a positive correction in sales for December.

Using a best-fit combination of the two models, we obtain a point forecast of 5.04 million units (SAAR), an increase of about 2.3 percent from November.

More details about the methodology for this month’s forecast can be found here.

The structural model suggests that, on average, an increase in interest rates is associated with an increase in home sales in equilibrium. Because interest rates fell in December along with signs of credit easing, an expected increase in home sales can be associated with larger positive changes in mortgage credit supply relative to mortgage credit demand. However, if interest rates had remained at their November level, thus suggesting a larger mortgage credit demand increase, the structural model would predict existing home sales to be 4.96 million units (SAAR), an increase of 0.6 percent.