Some people are born lucky, lucky enough to have parents able to help finance their higher education. And some people are doubly lucky, lucky enough to have parents able to help finance both their higher education and a down payment to buy a home.

Using data from the Federal Reserve Board’s 2014 Survey of Household Economics and Decisionmaking (SHED), Zillow estimated the extent of this “doubly lucky” population:

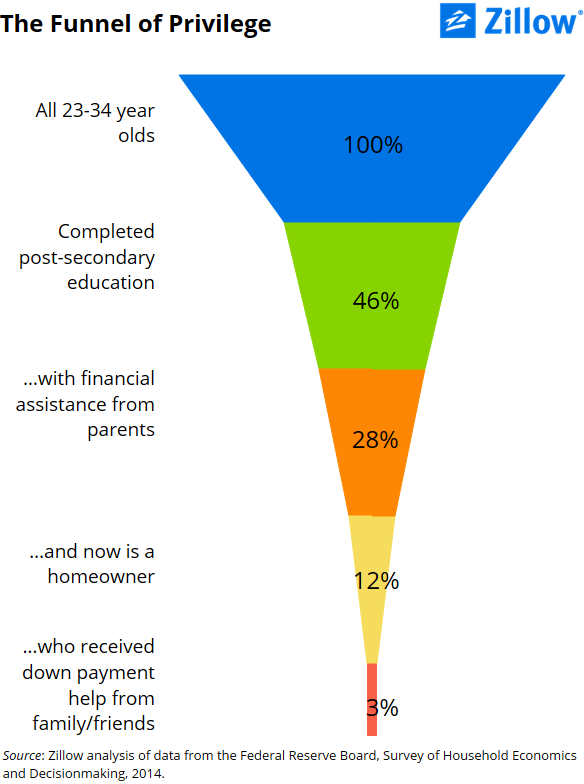

- Among young adults aged 23 to 34 (commonly known as millennials), 46 percent completed some form of post-secondary education – anything from an associate’s degree to a doctorate or professional degree.

- Of those who completed a post-secondary degree, 61 percent (or 28 percent of all young adults) received financial assistance from their parent(s), including cases where the parent(s) took out a loan to cover the child’s post-secondary educational costs.

- Of those who received financial support from their parents for post-secondary education costs, 43 percent are current homeowners. In other words, 12 percent of all young adults received parental support to fund their education, and have since bought a home.

- Among those who own their home and received financial support from their parents for their post-secondary education, 25 percent also received family support in funding their down payment.[1]

In total, 9 percent of all young adults who received parental support for their education also received family support in funding their down payment. Looking at the data in another way, 3 percent of all young adults received parental support for both education and buying a home.

Interested in running a similar analysis of the Federal Reserve’s SHED data? Zillow’s code is available here, and you’re welcome to use it as a starting point. We’re curious to hear what you find!

[1] The sample size associated with these five conditions – age, education, financing of education, current housing tenure and source of funding for a down payment – is small and should be interpreted with caution.