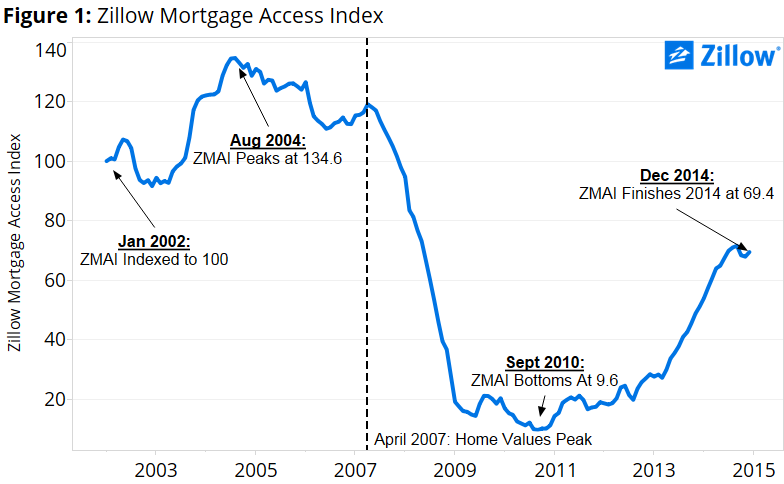

Despite Year-End Blip, 2014 Caps Strong Two-Year Period of Easing Mortgage Access

Despite a slight drop in the fourth quarter, the Zillow Mortgage Access Index (ZMAI) ended 2014 up 18.3 points from the end of 2013. At 69.4 points, ZMAI closed 2014 at its highest year-end value since Q4 2007, when it was at 97.8 points (and in the beginning stages of a years-long freefall).

This is the second publication of ZMAI data. ZMAI tracks seven monthly measures of mortgage availability and boils them down into a single metric to determine how easy it is to get a mortgage:

The index fell slightly (two points) in the fourth quarter compared to the third quarter, the first quarterly drop since the beginning of 2013 (figure 1).

While the magnitude of the quarterly drop isn’t large compared to very rapid overall growth since the beginning of 2013, the tapering-off may be a sign of credit conditions plateauing at what may become a new normal. Credit access at or near even 2002 levels may still be too risky for lenders living in the shadow of the housing market collapse.

Between the very end of 2012 and the end of 2014 (calendar years 2013 and 2014), ZMAI rebounded more than 41 points in total (figure 2). This is a promising sign of mortgage credit easing, and represents a stark divergence from the virtually nonexistent easing between 2009 and 2012. Over this four-year timespan, ZMAI grew a paltry 0.3 points, after plummeting 84.4 points from 2006 to 2007.

Four of the variables included in ZMAI account for more than 35 points of ZMAI’s growth the past two years (figure 3). A higher percentage of borrowers are taking out second mortgages compared to two years ago (4.6 percent of all mortgages then, 12 percent now). The lowest-end of credit scores of approved conventional borrowers was still north of 700 at the close of 2012, but likely fell below 675 by the close of 2014. Borrowers with low credit scores are also getting more offers in general, according to the Zillow Mortgage quotes ratio. Two years ago, borrowers with lower credit scores were only getting roughly a third of the quotes (36.4 percent) borrowers with impeccable credit scores were receiving; now that number is more than 50 percent.

Finally, lenders are underwriting more non-conforming loans to borrowers able to pay a 20 percent down payment on a home. At the end of 2013, only 6.3 percent of loans in this high down-payment market were non-conforming. Now, 9.6 percent of loans are in this category, the highest since 2007.

[1] The 10th percentile credit score of conventional mortgage borrowers (the credit score of borrowers at the low end of the approved credit score spectrum).

[2] The 90th percentile debt-to-income ratio of conventional borrowers (approved borrowers devoting the highest percentage of their income to debt payments).

[3] The spread between 30-year fixed-rate mortgages and the 10-year treasury rate.

[4] The proportion of loans with 20 percent or more down that are non-conforming (those that cannot be sold to a GSE, meaning the risk must remain on the lender’s books).

[5] Amongst loans where the borrower puts less than 10 percent down on their home, what percentage of borrowers went the route of private mortgage insurance (versus obtaining an FHA loan).

[6] The proportion of loans extended in a month that are second mortgages on a home, which includes borrowers who were able to get a second mortgage to cover part of their down payment requirement (sometimes referred to as a piggyback loan).

[7] How many quotes a Zillow Mortgage inquirer with a credit score between 600 and 640 receives compared to an inquirer with a credit score of 760 or higher (e.g., in December 2014, inquirers in the lower bucket received just over half the number of quotes that a borrower in the higher credit score bucket received).

{kind=link}